SPONSORED BY:

You already know that, for most, Q4 2025 isn’t shaping up to be business as usual.

Tariffs (need we say more?). Wavering consumer spending and confidence. Relentless margin pressure. Most operators are already very well aware that this year will require real-time decision-making.

That’s why we ran this survey — to understand how DTC brands are planning amidst the uncertainty of 2025.

This report is brought to you by DTC and Keen. Want to make better decisions and forecast with more clarity before the busiest ecommerce season of the year? Connect with Keen.

Below, we break down insights from over 600 responses — what brands are thinking, how they’re adapting, and where they’re heading next.

If you’re feeling the pressure, you’re not alone. This is the signal beneath the noise.

*Note: All data below has been filtered to include only responses from individuals who own, run, or work at a DTC brand.

Keen helps many DTC brands with their business planning, with a particular focus on optimizing marketing investments. They equip their clients to cut through economic uncertainty to recognize business drivers and confidently plan their business accordingly.

The current uncertainty is evident in how Keen’s clients are engaging in their platform. There has been a significant uptick in clients’ use of Keen’s scenario-planning platform to establish future marketing plans. Clients embracing this practice recognize there are many environmental factors they cannot control.

Scenario-planning serves as the means of quantifying best/worst case scenarios for these factors and then confidently planning what they CAN control – their marketing strategies.

DTC Newsletter is a daily weekday newsletter read by 155,000+ operators, founders, and marketers at ecommerce brands. We cover what’s new and what’s working in DTC. From strategy and performance trends to creative, tips and tactics, and platform updates, our content helps you stay informed and make better decisions, faster. We also host podcasts that dive into real-world lessons from brand operators, agency leaders, and marketers driving growth in ecommerce. Subscribe here to get insights in your inbox every weekday morning.

Only 15.41% of brands say their Q4 plan is locked and ready to go. Everyone else? They’re still figuring it out — adjusting in real time, just like the market demands.

58.11% told us they’re actively adjusting their strategy — which makes sense, given the uncertainty around tariffs, shrinking margins, and unpredictable spend.

About 1 in 4 are either scrambling or holding off entirely, waiting for more clarity before they commit.

Bottom line: Most brands aren’t following a set playbook this year. They’re staying flexible, reacting to what’s happening in the moment, and building plans that can shift if needed.

🚨 Deeper Insights from Keen:

So far this year, the average Keen customer has created 58 scenarios across their collective portfolios — nearly 2x the number modeled during the same period last year.

Total plans are up 163% year-over-year, while customer growth is up just 39%, pointing to a clear shift in how deeply brands are engaging with future planning.

Brands embracing this practice recognize that many of today’s biggest pressures — tariffs, costs, consumer unpredictability — are outside their control. Scenario planning helps quantify those unknowns, map out best- and worst-case outcomes, and make confident decisions about what is in their control: their marketing strategy.

When broken down by revenue band, nearly 74% of brands doing $10M+ say they’re actively shifting tactics for Q4 — the highest of any revenue band.

In contrast, only 48.86% of sub-$1M brands say the same, with 21.59% claiming they’re already locked in.

Roughly a third have kept their targets in line with last year (31.62%), while another third are aiming higher (30.27%) — showing that some are still betting on growth, despite the uncertainty.

But not everyone is feeling bullish. About 16% have already scaled back their targets, and another 22% haven’t finalized theirs at all — a sign that some teams are waiting to see how things will shake out before locking anything in.

It all points to a Q4 that still feels unsettled. For many brands, goal-setting is less about aggressive growth and more about staying realistic and responsive.

Mid-sized brands ($5M–$10M) are the most optimistic about growth. They represent the highest percentage (38.89%) across all revenue bands to have increased their Q4 targets.

Nearly half of brands say their pricing strategy and margins are the most vulnerable heading into Q4 — more than any other area. That tracks with rising costs, tighter budgets, and the pressure to stay competitive without burning profitability.

Profitability targets and ad spend effectiveness were the next biggest concerns, showing how the ripple effects are hitting both ends: what it costs to sell, and what you’re able to make back.

Inventory and fulfillment worries were less common, but still notable.

Only 11.08% of respondents said they’re insulated from these issues entirely. For most, something’s being squeezed — and margins are taking the brunt of it.

Only 28.11% of brands feel that margin pressure is minimal right now — the rest are feeling it in one way or another.

Nearly half (46.49%) describe it as noticeable, and another 18.92% feel it’s significant and are actively adjusting pricing or spend to manage the impact.

6.49% say it’s severe, with margin erosion becoming a real threat to profitability.

The takeaway? While it’s not a crisis for everyone, margin pressure is clearly shaping how most brands approach Q4 — whether that means rethinking discounts, shifting channel mix, or getting leaner with operations.

🚨 Keen’s Additional Insight:

Margin pressure hits smaller brands harder. Keen data shows that brands under $50M consistently reinvest 25–35% of their revenue into marketing, compared to just 2–3% for billion-dollar brands. When costs rise — whether from tariffs, supply chain shifts, or ad rate spikes — these brands have far less cushion. Every dollar matters more, making them more vulnerable to even modest margin erosion heading into Q4.

55% of $10M+ brands say margin pressure is noticeable, the highest of any group.

Only a small percentage in any given group describe the situation as severe.

The most common answer? Brands are still evaluating. Over 40% haven’t locked in a clear margin-preservation strategy yet — which reinforces just how uncertain the landscape is heading into Q4.

Among those taking action, cost-cutting is the go-to move (39.73%), followed by reducing or reallocating ad spend (34.59%) and raising prices (31.89%).

It’s clear that many teams are looking for fast, controllable levers to pull.

Retention-focused plays and new high-margin products were less common, suggesting that longer-term strategies are taking a back seat to short-term survival tactics.

It’s not about bold moves right now — it’s about measured, tactical reactions to a tough environment.

45.45% of brands under $1M are still evaluating options, compared to just 30% of $10M+ brands, who are more likely to have already made tough calls, like cutting costs (46.25%) or reducing ad spend (41.25%).

Less than 7% of brands said that they’re highly confident in their Q4 forecasts.

39.19% are leaning on recent data trends and feeling moderately confident, while 34.05% say their forecast is more directional than dependable.

And 1 in 5 brands openly admitted they’re guessing right now — a clear signal of just how murky things feel.

Planning isn’t off the table. But precision? That’s a luxury most brands don’t have this year.

50% of brands doing $5M+ say they’re moderately confident and relying on recent data trends, compared to just 32.39% of sub-$1M brands.

Smaller brands are far more likely to say they’re guessing — coming in at over 10% higher than any other group.

Only 20.27% of brands have fully modeled contingency plans for a softer Q4.

The largest group — 41.62% — say they’ve discussed backup plans but haven’t formalized anything. That tells us most teams feel as though a slowdown is possible, but haven’t committed time or resources to fully map out a plan B yet.

Another 15.68% are holding off until they have more clarity, and 22.42% are locked in on their core plan.

It’s a bit of a gamble. With so much volatility this year, not having a defined “what if” strategy could make Q4 even harder to navigate if demand drops.

The biggest shift this year? Focus. Nearly 50% of brands are either doubling down on what’s worked before or investing more heavily in high-performing channels — a clear signal that teams are prioritizing predictability over experimentation.

17.30% have pulled back on testing altogether, and nearly a quarter (23.51%) are cutting spend across the board. That reflects a cautious mindset — likely tied to pressure on margins and lack of forecasting confidence.

Very few are reallocating channels or deferring spend entirely, suggesting most brands still see Q4 as a critical moment… they’re just approaching it with sharper, more selective budgets.

🚨 Keen’s Additional Insight:

This caution is exactly what we see in budget splits on Keen.

According to Keen’s platform data from 2025, smaller brands, especially in Retail & Ecom and Health & Beauty, keep 50–60% of their marketing budgets locked in direct conversion channels, like Paid Search, Paid Social, and Retargeting.

In an uncertain Q4, that shift gets even sharper. Rather than risk spend on brand-heavy or experimental plays, they channel more into tactics with immediate, measurable returns — often delaying new tests or broader awareness pushes until conditions stabilize.

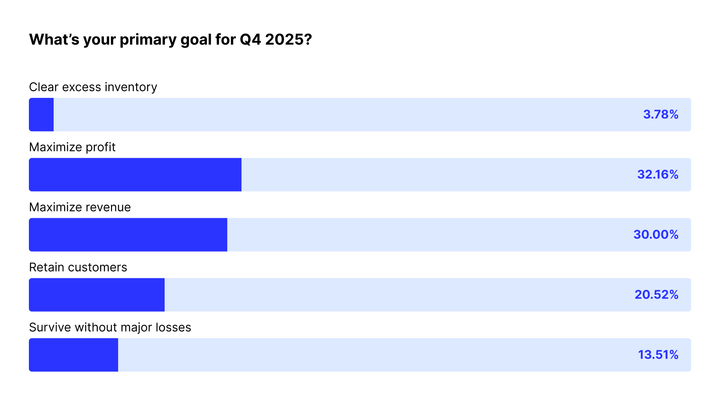

When asked about their primary Q4 goal, most brands are split between profit (32.16%) and revenue (30%) — showing a nearly even divide between those focused on staying lean vs. those chasing topline growth.

Another 20.52% are focused on retention, suggesting some brands are playing the long game, even in a tough year.

Meanwhile, 13.51% just want to make it through without major losses — a reminder that for a meaningful portion of the industry, making it through in one piece is the most realistic win.

Only a small number (3.78%) are focused on clearing inventory, signaling that most brands are more concerned with financial performance than operational cleanup this season.

41.25% of $10M+ brands say maximizing profit is their #1 goal for Q4 — the top response in that revenue band.

Q4 2025 is shaping up to be anything but predictable—and most DTC brands are adjusting accordingly. From shifting performance targets to scenario planning and margin preservation, it's clear that flexibility and focus are the name of the game this season.Big thanks to Keen for sharing their additional insights with us on this timely report and helping brands plan with more confidence amid the uncertainty.

👉 Want to explore how Keen can help you scenario plan for Q4 and beyond? Learn more here.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)